In the complex ecosystem of South African insurance, the “Expert Report” is often treated as the final word—a scientific gavel that falls to justify the rejection of a motor claim. For many policyholders, receiving a report filled with physics formulas and technical jargon feels like an insurmountable wall.

However, after years of investigating losses within this industry, I have seen behind the curtain. What is presented as “independent expertise” is frequently a thin veneer for advocacy. There is a systemic issue in South Africa where so-called independent experts have morphed into de facto employees of insurers, seeing their role not as finders of fact, but as protectors of the insurer’s bottom line.

The Conflict of Interest: A Crisis of Independence

The imbalance of power begins with the contract. Many insurers require investigators to sign Service Level Agreements (SLAs) containing language such as, “The investigator shall act in the best interest of the insurer at all times.” I have personally declined lucrative work from major insurers because of this exact clause. My stance is simple: an investigator cannot be “objective” while contractually bound to “interest.” I have requested amendments to these SLAs to allow for the pursuit of objective facts, regardless of whether those facts favor the insurer or the claimant. Most insurers refuse.

This creates a “captured” industry of experts who rely on a single insurer for the vast majority of their billable hours. If they don’t find a reason to reject a claim, the work dries up. The result is a litany of “Expert Reports” riddled with scientific flaws, biased interpretations, and legal overreach.

The Anatomy of a Flawed Expert Report

To understand how claims are unfairly rejected, one must look at the specific, recurring failures in the reports currently being produced in the South African market.

1. The Death of Scientific Rigor

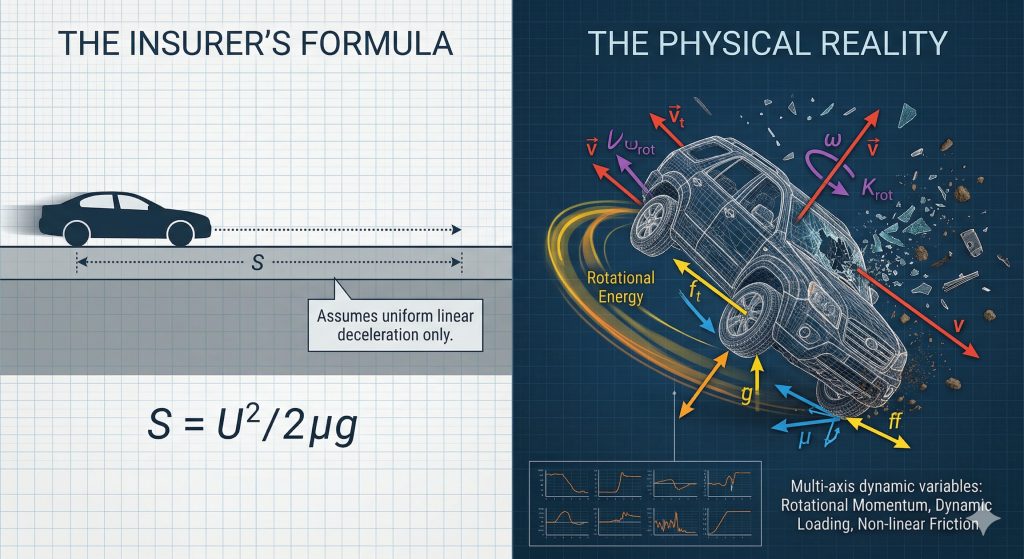

The most common weapon used against a claimant is the “Speed Calculation.” However, these calculations often fail the basic requirements of scientific methodology:

- Estimated Friction Values: Experts frequently base velocity calculations on estimated coefficient of friction values (e.g., $0.6\mu$) rather than conducting empirical skid tests on the specific road surface.

- Missing Formulas and Margins of Error: Reports often state a definitive speed—for example, “134 km/h”—without showing the underlying physics formulas or accounting for a margin of error. In science, an absolute number without a standard deviation is a red flag.

- The “Generic Chart” Trap: Instead of factoring in the specific weight and braking system of the actual vehicle, “experts” often rely on generic, illustrative stopping distance tables to definitively claim a driver could have stopped in time.

- Linear Math for 3D Crashes: A major mistake is using a simple “skid-to-stop” formula for a crash that involved a rollover. A rollover sequence dissipates energy through rotation, vehicle deformation, and airborne phases—none of which are accounted for in a linear braking formula.

2. Methodological “Shortcuts” and Rhetoric

In forensic reviews, I have identified a trend where experts use “one-size-fits-all” math to create a false sense of certainty:

- The “Percentage” Rhetoric: Experts often report speed as a “percentage above the limit” (e.g., “73% over the limit”). This is a rhetorical tool, not a scientific one. A vehicle traveling at $160$ km/h has the same physics regardless of the regulatory speed limit.

- Ignoring Human Factors: Reports often focus exclusively on speed while ignoring external influences, such as a following vehicle with bright headlights that may have caused glare or visual impairment.

3. Ephemeral Evidence and Data Spoliation

The integrity of an investigation depends on the quality of the data collected, which is often compromised in the South African context:

- Delayed Inspections: Scene inspections are often conducted long after the crash, leading to the loss of crucial ephemeral evidence like tyre yaw marks.

- The “Missing” Field Notes: When requesting primary evidence, we often find that original photographs were discarded, and raw measurement records or field notes “do not exist”. Without these, the report cannot be independently verified or reproduced.

- Pre-Planned Spoliation: Some reports explicitly state that evidence collected from the vehicle will be systematically destroyed after a short period, preventing the insured from conducting an independent verification.

The Institutional Layer: Transparency Without Power

The systemic failure of insurance investigations is compounded by a second layer: the breakdown of institutional transparency. Even when policyholders seek to challenge the fairness of the system, they are met with a “transparency regime” that often fails to provide the data necessary for accountability.

The Resistance to Statistical Truth

Efforts to scrutinize patterns within the National Financial Ombud Scheme (NFOS)—meant to be an impartial referee—have faced significant resistance. When independent analysts attempt to verify the objectivity of the ombud process using the Promotion of Access to Information Act (PAIA), the institutional response often follows a pattern of delay and contradiction:

- The Confidentiality Defense: Institutions frequently claim that even anonymized, statistical data is protected by confidentiality. The Information Regulator has dismantled this defense, ruling that aggregated data is purely statistical and not confidential.

- The Resource Constraint Argument: Organizations may claim that fulfilling data requests would “overwhelm” their staff. The Regulator has found that requests for statistical information should be feasible through efficient data processing.

The Enforcement Gap

The most critical failure is the administrative backlog that follows a legal victory. A citizen can invoke PAIA, win a favorable ruling from the Information Regulator, and still fail to receive the records due to “institutional drag” and delays that can last for years. This “exhaustion” strategy means the public has a formal right to ask for information, but no timely right to receive it.

Restoring Balance to the Industry

The current dynamic is grossly imbalanced. Insurers have deep pockets to hire “experts” who function as advocates, while the average claimant cannot afford a counter-expert to point out that the insurer’s report is scientifically hollow.

Expert evidence should be an aid to reach the truth—not a weapon used to save an insurer money. Until we move away from “Interest-based” SLAs and back toward “Fact-based” investigation, and until institutional enforcement is swift and effective, the integrity of the South African insurance industry will remain in question.

If you are a claimant facing a rejection based on a technical report, remember: just because it looks like science doesn’t mean it is. Every variable, every formula, and every “estimated” value is a point of potential failure that deserves to be challenged.

By Stan Bezuidenhout